Chipmakers lead Tech to more all-time highs

Jamie Dutta >

Jamie Dutta >

Jamie Dutta is a Market Analyst for Vantage. He comes with extensive experience as a full-time trader and financial market commentator, having worked as a trader in top tier investment banks and trading houses.

* Trump weighs military action against Iran with ceasefire ‘on life support’

* Crude prices jump 4% initially but pares gains as tensions stay high

* Some UK cabinet members could confront Starmer at meeting today

* Fresh record S&P and Nasdaq highs as AI enthusiasm offsets Iran stalemate

FX: USD was relatively quiet and printed an inside day even as geopolitical tensions ramped up. President Trump strongly rejected Iran’s response to his peace proposal and said the ceasefire was on ‘life support’. Looming over this is the Trump-Xi meeting later this week where it was presumed a deal was needed ahead of these historic talks. This week’s low in the DXY sits at 97.62. The dollar would typically rebound on any re-escalation while stock market performance has been highly correlated currently to dollar crosses. We wrote about this push-pull theme in the Week Ahead. Today brings US CPI with central bankers squarely focused on price pressures and second round effects, especially after Friday’s second straight headline NFP beat.

EUR has been choppy for a few weeks trading between 1.17 and 1.18. Prices need to get above the 61.8% Fib of this year’s high to low move at 1.1825 to see a bull move towards 1.19 and 1.20. The prospect of ECB rate hikes is underpinning support for the single currency, as the outlook looks muted with activity data poor. ECB speak this week is likely to be hawkish with President Lagarde and Lane speaking on Wednesday. There’s around an 80% chance of a June 25bps rate rise.

GBP grabbed lots of headlines but was mid-pack amid its peers. Pressure on PM Starmer ratcheted up as an increasing number of Labour MPs voiced their desire for a new leader. A total of 81 are needed to kick off a leadership contest, though senior members of the cabinet are yet to put their names into the hat. There is actually a cabinet meeting today which some Westminster watchers believe could be the beginning of the end. That could mean the shortest reign of a labour PM in history. But GBP and Gilt yields haven’t moved even as betting markets see an 80% chance of Starmer not being in office by the end of the year. The 100-day SMA is 1.3477 with the 50-day and 200-day at 1.3419/20.

JPY was the major underperformer as the pair rose up to the 100-day SMA at 157.35. Key today is US Treasury Secretary Bessent’s meeting with Prime Minister Takaichi, Finance Minister Katayama, and BOJ Governor Ueda with the weak yen on the agenda. Japan and the US reaffirmed their commitment to close coordination after the G7 meeting in April. Bessent is unlikely to restrain the Japanese government’s response, while he could give some kind of signal about monetary policy like he did last October.

US stocks: The S&P 500 added 0.18% to close at 7,412, the Nasdaq closed up 0.29% at 29,321 and the Dow Jones settled higher by 0.19% at 49,704. Six sectors were positive and five in the red with Energy, Materials and Industrials all up more than 1%. Communication Services was the biggest laggard by far, off 2.34% as Alphabet, Meta, Netflix and Disney all closed lower on the day. The former explored its first yen bond sale for AI expansion. The SOX semiconductor index hit more record highs as Micron, Qualcomm and other chipmakers continued their parabolic melt-up. Chip demand is surging thanks to the AI buildout and supply is more limited than expected, potentially exacerbated by the Hormuz shutdown. Next year’s earnings for these stocks have almost doubled for next year, which means the ‘picks and shovels’ for data centres have outperformed the Mag Seven and hyperscalers since ChatGPT launched.

Asian Stocks: Futures are mixed. APAC stocks traded mixed after the solid NFP data and better than expected China data, offset by rising Middle East tensions. The ASX 200 fell on heavy losses in health as CSL shares slumped 19%. The Nikkei 225 posted fresh record highs above 63,000 but then reversed gains on higher oil prices and weak earnings outlooks of Nintendo and Honda. The Shanghai Composite and Hang Seng were varied with mixed tech performance and stronger data helping the mainland.

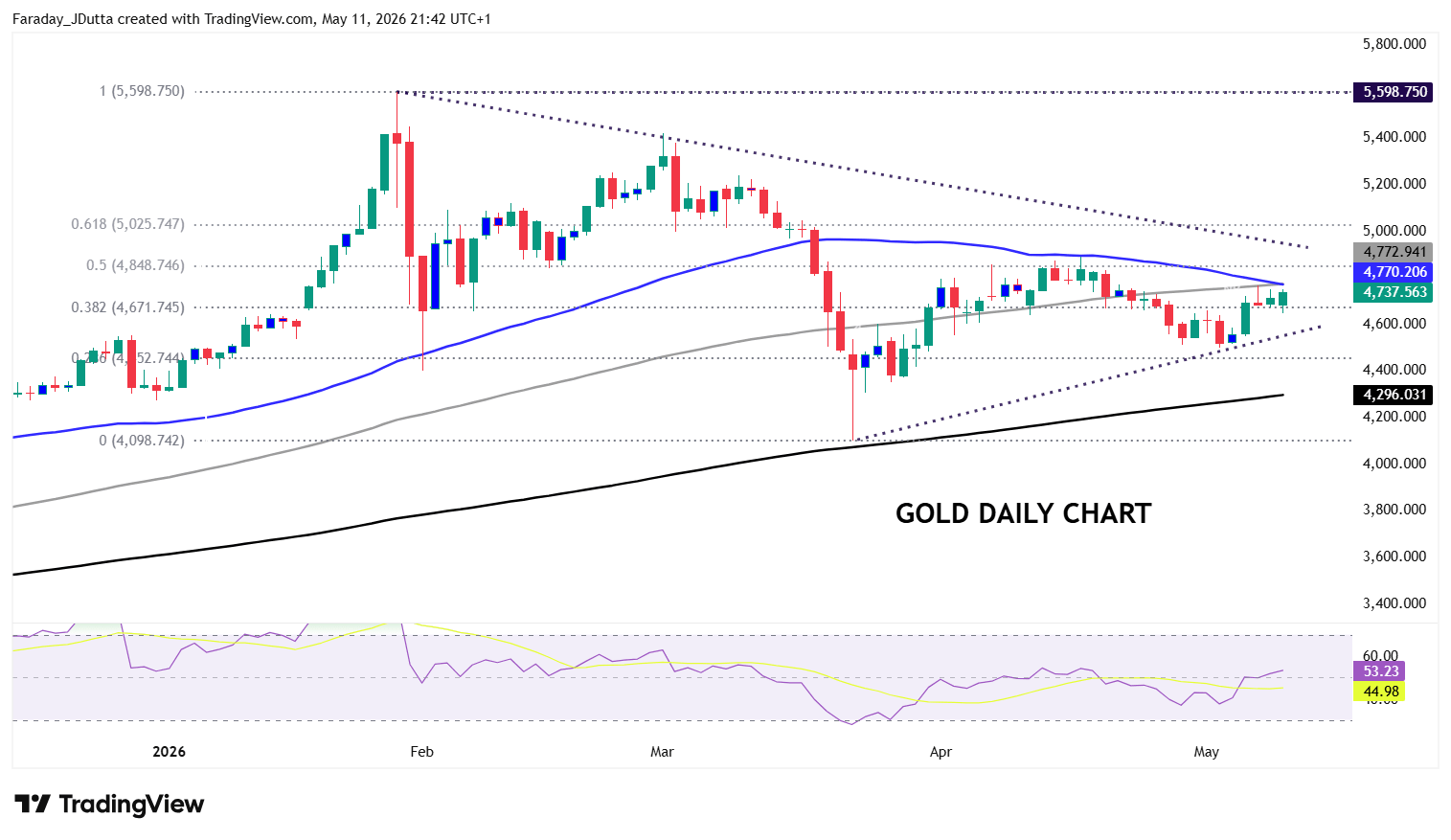

Gold ticked higher for a second day in a narrow range, with a huge triangle pattern forming. See below for more.

Day Ahead – US CPI

April headline inflation is forecast to rise 0.6% m/m and 3.7% y/y in April from 0.9% and 3.3% respectively. Core, which strips out volatile food and energy prices will print modestly higher than prior at 0.3% from 0.2% and 2.7% form 2.6%. The March annual headline reading was the highest since May 2024, lifted by the war-driven energy shock as prices jumped 10.9% in March led by a 21.2% surge in gasoline.

The Fed will focus on secondary passthrough, which may take some time to show up, and if the shock feeds into consumer demand. At the April FOMC meeting, three dissenters voted against including any easing bias in the statement, arguing that inflation risks had risen enough for the Fed to keep all options open, including holding rates for longer or even hiking, rather than signaling an easing bias. This might be a message to incoming Chair Kevin Warsh, who has previously endorsed lower rates and tighter balance sheet policy. Another key shift in the Fed April statement was on inflation, with hawkish tweaks to the wording being caused by the recent surge in global energy prices.

Chart of the Day – Gold sideways for now

Gold edged higher to kick off a busy week on signs of renewed buying interest, supported by ongoing central bank demand and persistent geopolitical risks in the Middle East. China’s central bank remains a key structural support, and ongoing broad central bank demand has helped underpin market sentiment, even as some buyers have recently turned to gold sales to support domestic currencies. While recent US-Iran military escalation has lifted haven demand, gains have been limited by a still‑restrictive macro backdrop, with elevated real yields, a firm US dollar, and reduced expectations for near‑term Fed rate cuts continuing to cap the upside. The chart is forming a big triangle, and the 200-day has held since 2023, so around 4,300 should be strong support. Upside above 5,000 targets 6,000 with at least a retest of 5,400. The 50-day and 100-day SMAs sit at 4,769/72.