Markets in risk-off mode into Nvidia earnings

Jamie Dutta >

Jamie Dutta >

Jamie Dutta is a Market Analyst for Vantage. He comes with extensive experience as a full-time trader and financial market commentator, having worked as a trader in top tier investment banks and trading houses.

* President Trump threatens to attack Iran, says they want a deal

* NATO considers Strait of Hormuz deployment to protect ships

* US stocks slide under pressure from higher interest rates

* Gold and silvers prices fall as oil shock sends yields soaring

FX: USD rose to near 6-week highs as it bounced off support around the 50-day SMA at 98.99. US Treasury yields continued to push higher with the 10-year breaking to fresh cycle highs at 4.66%, a level last seen in January 2025. There’s now a 60% chance of a rate hike before year-end, with a 35% chance in November. Those odds were near zero, one month ago. Persistently elevated oil prices and little sign of Iran yielding are impacting sentiment and boosting the greenback. A move above the January high means bulls would next target above 100.

EUR was mid pack among its peers again but the major broke down to fresh 6-week lows. A minor Fib level of this year’s high to low sits at 1.1569. Sentiment is deteriorating considerably, adding to the single currency near-term headwinds. Rising yields points to imminent ECB action and rate hikes in order to avoid losing control of the long end of the bond curve. There’s nearly three 25bps moves priced in for 2026, and until the Strait of Hormuz reopens, policymakers will need to remain hawkish.

GBP outperformed most of its peers, but prices fell below the 50 and 200-day SMAs at 1.3422/25. We got the first of this week’s data blitz with dire job numbers featuring rising unemployment, much lower payrolls and falling wage growth. That doesn’t paint the picture of major second round effects from the upcoming energy shock. But markets still price in nearly three 25bps rate hikes. On the domestic politics front, Andy Burnham’s pledge to maintain existing fiscal rules if he were to assume leadership of the UK Labour Party went down well with markets.

JPY weakened for a seventh straight day as the major rose above the 50-day SMA at 158.76. Widening US-Japan interest rate differentials have been hurting the yen and even an upside GDP surprise and better revisions were no real help. Markets price in a high chance of a rate hike at next month’s BoJ meeting but USD/JPY has limited resistance ahead of the psychologically important 160, which is of course intervention territory. There was a fair amount of jawboning from various officials.

US stocks: The S&P 500 lost 0.67% to close at 7,354, the Nasdaq closed down 0.61% at 28,819 and the Dow Jones settled lower by 0.65% at 49,369. Sector performance saw six sectors in the red and five positive. Healthcare, Energy and Utilities were the biggest gainers, while Materials, Communication Services, Consumer Discretionary and Financials were the major laggards. This points to rotation amid the sectors with eyes on Nvidia’s results released after the US close today. Akamai closed lower 6.3% after it announced a $2.6 billion convertible bond offering, highlighting rising worries about debt-fuelled AI growth. Home Depot beat on the top and bottom lines and back its full-year guidance as the stock closed marginally higher on the day.

Asian Stocks: Futures are mixed. APAC stocks traded mixed on US-Iran headlines and news that the US planned attack was put off. The ASX 200 saw strength in the consumer, telecom, real estate and financial sectors, while the RBA’s May meeting minutes noted that financial conditions would be somewhat restrictive after the May hike. The Nikkei 225 swung between gains and losses with the weak yen but stronger than expected GDP in the spotlight. The Shanghai Composite and Hang Seng were rangebound with few fresh drivers.

Gold dipped to new 6-week lows as rising US Treasury yields and the dollar hurt bugs. Silver fell over 5% on the day.

Day Ahead – UK CPI, FOMC Minutes

UK headline is expected to fall to 3.0% from 3.3% and core is forecast to rise 2.7% from 2.6%. April services inflation is predicted to ease to 3.5% from 4.5%. The declines are due to base effects weighing on the annual metric, as household energy bills dropped on account of government action in the 2025 budget. The early Easter period may also be a drag though rising fuel prices will offset this. All in, it’s a mixed picture but prices will remain well above the BoE’s 2% target, very different from just three months ago when officials were predicting a decline to around that goal in April.

The Fed meeting was Jerome Powell’s final one and likely to show growing support within the FOMC to drop its easing bias. The split vote was unusual and historic, and possibly a signal to the incoming Chair Warsh who is expected to want to cut rates early in his tenure. But the minutes are likely to shine a light on the hawkish dissent and vote, with inflation data like CPI and PPI only going in one direction at the moment.

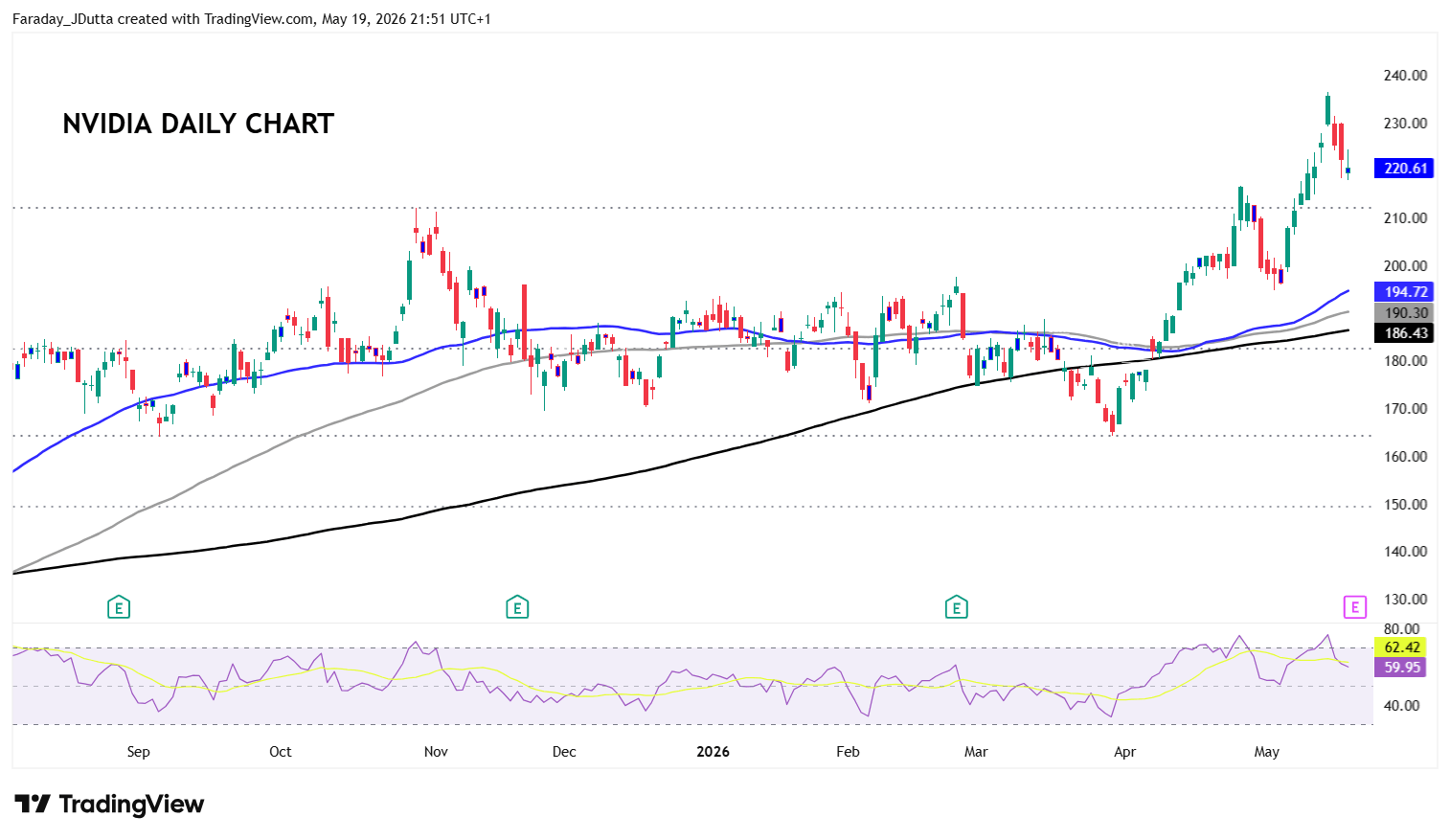

Chart of the Day – Nvidia reports after record highs

The world’s biggest company by market cap ($5.5 trillion) reports its latest earnings after the US close. This is essentially a live check on whether the AI boom remains intact. For this quarter, adjusted EPS is seen at $1.78 and revenue at $78.98bn and for the next quarter, profit and revenue are projected at $1.96 and $96.78bn. The giant chipmaker exceeded revenue expectations in all prior four quarters, so a beat is expected. Key will be forward guidance for the next quarter. That will show how much hyperscaler spending Nvidia is capturing, data center revenue growth and demand from its major cloud customers. Multiple hyperscalers have recently raised their projected capital expenditures for 2026. But Meta and Microsoft are both investing in custom AI chips while Broadcom is capturing more of the market. Any updates on China restrictions, AI demand trends, or supply constraints will also be in focus. Nvidia stock has surged recently, rising 20% in 2026 to fresh record highs. Options mkts see around a +/- 6% move on Thursday morning. We note that the stock dropped over 5% last time on profit-taking, concerns around stretched valuations and the market’s ever-rising expectations for Nvidia’s growth. The recent record top is $236.54 with the swing high from October 2025 below at $212.19.