Stock indices higher with Trump/Xi talks constructive

Jamie Dutta >

Jamie Dutta >

Jamie Dutta is a Market Analyst for Vantage. He comes with extensive experience as a full-time trader and financial market commentator, having worked as a trader in top tier investment banks and trading houses.

* US-China relations depend on Taiwan, Xi warns Trump

* GBP hits one-month low as PM Starmer braces for leadership challenge

* Fresh record highs in US stocks as NVDA cleared for H200 chip sales to China

* Crude oil steady amid continuing Hormuz crisis, Trump-Xi meet

FX: USD rose for a fourth straight day through both the 100-day and 200-day SMAs sat 98.65/52. The 50-day sits above at 98.97. US retail sales rose in line at 0.5%, with higher gasoline prices helping as the data are nominal dollar figures. The numbers point to ongoing resilience and little sign that higher gasoline costs are forcing consumers to cut back spending, even if consumer confidence is meant to be at record lows. The Trump/Xi summit appeared constructive – see below for more.

EUR dipped for a third straight day and through the 200-day SMA at 1.1681. ECB rate expectations are little changed with around an 80% chance of a June quarter point hike and a cumulative 70bps by year-end. Yield spreads between EZ and US have stabilised since the pullback from late April and should offer some fundamental support.

GBP was the big underperformer on the day and closed on its lows below the 50 and 200-day SMAs at 1.3428 and 1.3422. GDP beat estimates but seasonality is a big issue for the UK economy with Q1 consistently solid in recent year but then fading through the year. However, the key driver for the pound has been a plethora of headlines about leadership challenges with the Health Secretary resigning and an MP vacating his seat for another candidate, Andy Burnham to potentially take up. Betting markets give him a 43% chance of being the next MP. And he is the first choice of two-fifths of Labour members. Sterling reacted sharply to that news as he is seen as the most left-wing possible leader. That said, UK borrowing costs held up, and with yields steady and the 10-year just above 5%.

JPY headed towards the 50-day SMA at 158.70 with the major rising for a fourth day in a row and the daily RSI modestly above the neutral zone of 50. Yield spreads have widened so offering a headwind to the yen, though BoJ comments have been hawkish. There was some talk of intervention after spot prices sharp drop from 158.15 to 157.25.

US stocks: The S&P 500 added 0.76% to close at 7,501, the Nasdaq closed up 0.73% at 29,580 and the Dow Jones settled higher by 0.75% at 50,063. Sector performance saw six sectors in the green, with Tech the biggest winner, and Energy and Utilities also outperforming. Materials, Real Estate and Consumer Discretionary were the main laggards. Nvidia jumped 4.4% after CEO Huang said China meetings were “excellent” with some media reportedly approving 10 Chinese firms to buy H200 chips. Cisco surged 13.4% after it reported an EPS and revenue beat, and issued stronger-than-expected guidance. This highlighted surging AI infrastructure orders despite announcing job cuts. Ford jumped another 6.7% as demand remained strong after announcing its new battery systems business for utilities and data centres.

Asian Stocks: Futures are in the green. APAC stocks traded mixed with markets choppy and focus firmly on the Trump-Xi summit. The ASX 200 was muted with resilience in financials offset by tech, healthcare and energy lower. The Nikkei 225 hit fresh record high before paring gains. The Shanghai Composite and Hang Seng were mixed with Alibaba and Tencent earnings in focus, with AI projections boosting the former even though sales disappointed.

Gold fell for a third straight day and remained below the 50-day SMA at 4,679. Treasury yields and the dollar were higher, with above a 41% chance of a rate hike by year end. India, the world’s second-largest gold consumer, more than doubled import tariffs on gold and silver. This is part of efforts to support their currency and ease pressure on FX reserves as the Iran conflict drags on. It is likely to be a short-term headwind for physical gold demand in India.

Day Ahead

We reiterate what we said yesterday about the Trump-Xi summit. Constructive outcomes have seen headline‑driven progress built on tactical, transactional deals rather than broad, structural breakthroughs. That is especially the case given Trump’s shortened visit. Outcomes are centred on economic and trade issues, with ‘winners’ on both sides. Certainly, conciliatory headlines, among Presidents Trump and Xi bolstered risk assets and stocks like NVDA which has been front-running some of this already.

But oil prices only moved modestly lower on headlines around China playing a more active role in pressuring Iran towards a peace deal. Trump did say Xi will not give military equipment to Iran. This week’s hot CPI and PPI data still linger over the market while Treasury yields are at important recent highs ie. 4% in the 2-year, 4.5% in the 10-year and 5% in the 30-year. The resilience of the US consumer was also evident in retail sales figures though the longer the Middle East war continues, the more activity will likely stall.

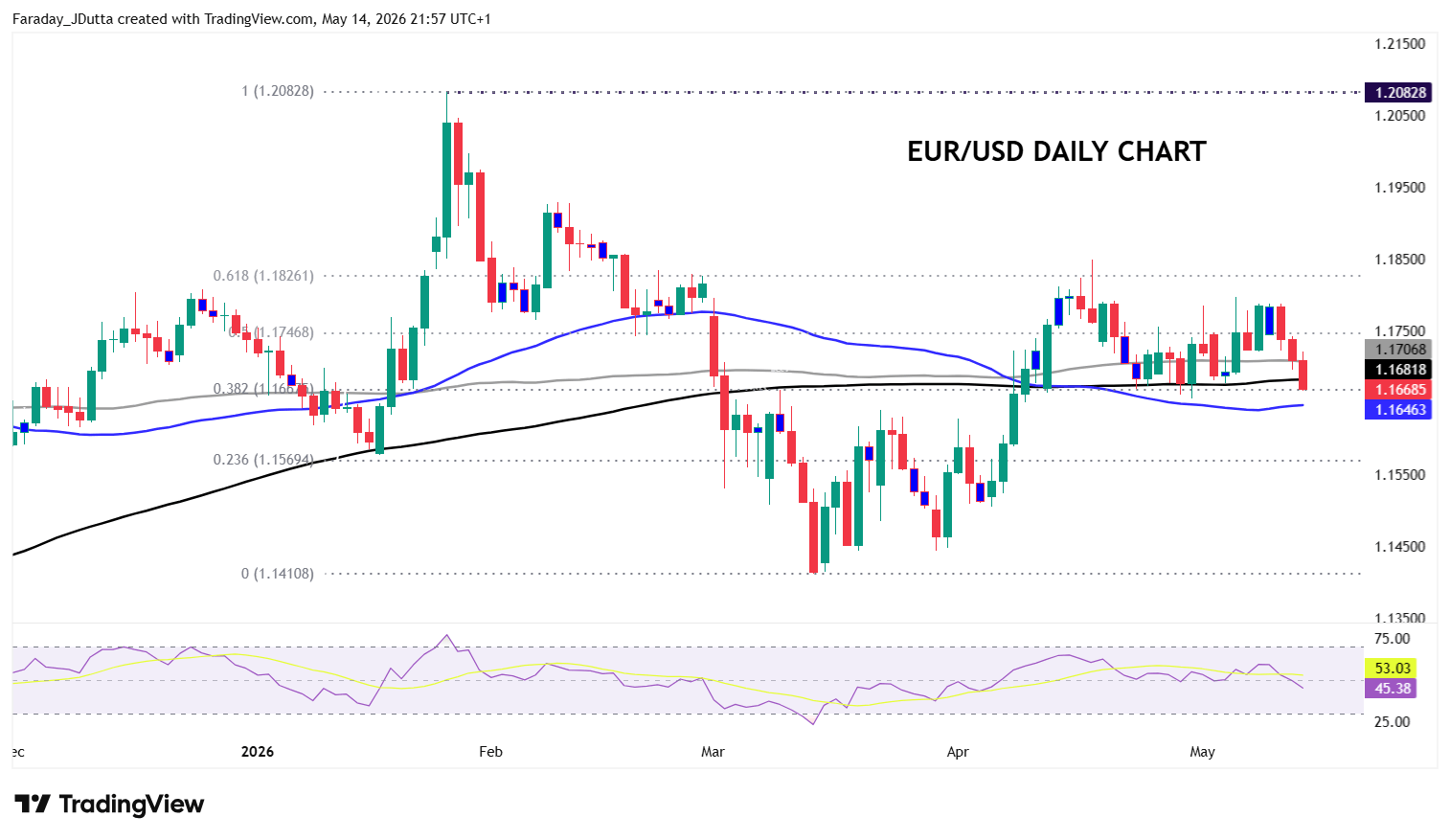

Chart of the Day – EUR/USD breakdown?

The world’s most popular currency pair has fallen below the 200-day SMA at 1.1681. This is the first time in five weeks this has happened, after a period of range trading between 1.16 and 1.18. The daily RSI has slid below 50, suggesting potential bearish momentum. Prices are now also at the bottom of some key Fib levels drawn from the January-March decline. Support sits around the 38.2% level at 1.1667 and resistance above is around the 61.8% level at 1.1826. Congestion has centred around the midpoint at 1.1746. More selling could encounter next support at the 50-day SMA at 1.1646, with the minor Fib level at 1.1569.