Dovish Fed refuels “Everything Rally”, ECB and BoE next up

Headlines

* FOMC holds rates steady and sees cuts next year

* Dollar plunges, stocks hit new highs as Powell pivots

* ECB set for second straight hold as markets wait for dovish turn

* Gold surges nearly 2.5% as Treasury yields and USD fall

FX: USD fell 0.86% after the Fed shocked markets by signalling a new cycle of policy easing was set to take place in the new year. The updated median dot plot revealed 75bps of rate cuts in 2024. Powell then talked dovishly at his press conference reinforcing the pivot to come. The odds for a March rate cut doubled to near 80% after the meeting. A total of approximately 114bps are priced in for 2024. The dollar is eyeing up the November low at 102.46 with a major Fib level at 102.54.

EUR jumped versus the dollar to the next resistance above at 1.0862. The major sat below the 200-day SMA at 1.0826 before the FOMC announcement. Focus now turns to today’s ECB meeting which is expected to not support the current rate cuts seen in the euro curve.

GBP was the underperformer after dismal GDP data at the start of yesterday. Cable printed a low of 1.2501 which touched the 200-day SMA. The move was then reversed on the back of the weak dollar post-FOMC. Prices closed above next resistance at 1.2589.

USD/JPY plummeted 1.77% as Treasury yields sunk. The major closed near its lows and just above a support zone around 142.47. The 10-year US Treasury dropped a huge 18bps on the day and is now sitting on its 200-day SMA just above the psychological 4% level.

AUD advanced higher, up over 1.5% and near to recent highs around 0.6659. NZD spiked above 0.62 before paring gains. Kiwi Q3GDP contracted sharply, printing at -0.3% versus +0.2% expected.

Stocks: US equities went into overdrive hitting new cycle highs. The S&P 500 added 1.37% to settle at 4707. The tech-heavy Nasdaq 100 finished 1.27% higher to close at 16,562. The Dow moved up 1.40% at 37,090.The S&P 500 and Nasdaq hit fresh closing highs for the year. All sectors in the S&P 500 closed higher. The blue-chip index is now up 22.6% for the year, while the Nasdaq is up over 40%. The Dow made a new record high for the first time in nearly two years. It is up 11.9% in 2023. The small cap Russell 2000 index shot up 3.5% on the day.

Asian futures are in the green. APAC stocks traded mixed on Wednesday. The Nikkei 225 was supported by an encouraging Tankan survey. Sentiment was at its highest since March 2020 for large manufacturers. The ASX 200 saw strength led by healthcare after a surge in Sigma shares.

Gold rocketed higher on the dovish tone from the Fed and Chair Powell. The expected push back didn’t happen with rate cut bets increasing and yields moving sharply lower, which dragged down the dollar.

Day Ahead – ECB and BoE Meetings

Both the ECB and Bank of England will keep rates unchanged at their meetings later today. The BoE gathering is a statement-only affair which means there is no press conference or quarterly new economic forecasts. That could result in slightly less volatility as the chance to direct the messaging will be fairly limited. In any event, the MPC are likely to keep a hawkish bias similar to their last meeting. Rates will be kept restrictive for an extended period of time due to still high inflation and wage growth.

The ECB will probably want to push back against rampant rate cut bets. These were increased after the recent surprise downside miss in inflation and less hawkish comments from some ECB hawks. With over 115bps of easing priced in by markets, and the first cut in the first quarter, it will still be a shock if President Lagarde endorses this at all.

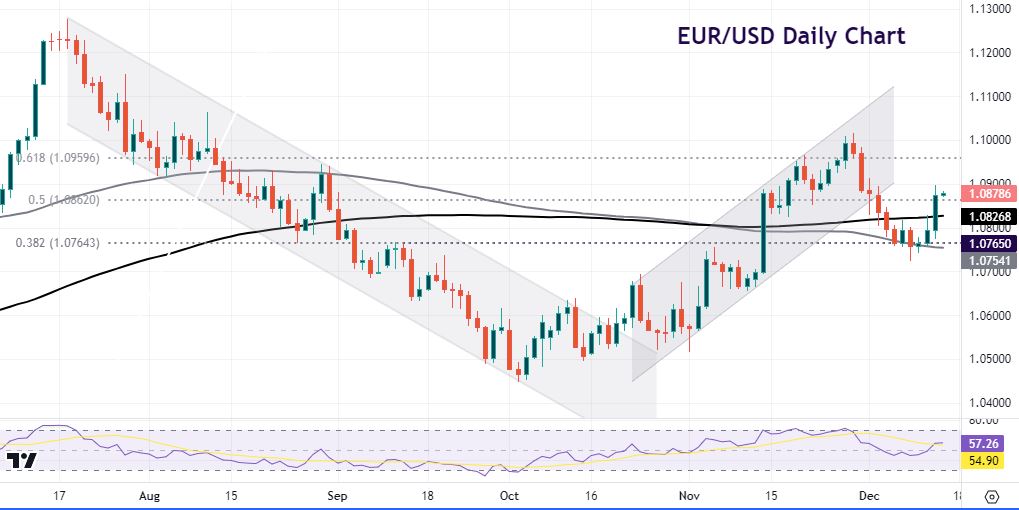

Chart of the Day – EUR/USD bounces off support

The world’s most popular currency pair had been tracking sideways for a few days, which is unsurprising in the days leading up to the high-risk events on this week’s calendar. But the more price action compresses, the bigger the range expansion will eventually be.

Support had been found at a major Fib level of the summer rally at 1.0764. The 100-day SMA is just below here at 1.0754. The major surged during and after the FOMC meeting. Yesterday’s move breached the 200-day SMA at 1.0826 and the 50% mark of the summer move at 1.0862. November highs sit above 1.10.