Crude, USD up, stocks down ahead of Fed & big tech results

Jamie Dutta >

Jamie Dutta >

Jamie Dutta is a Market Analyst for Vantage. He comes with extensive experience as a full-time trader and financial market commentator, having worked as a trader in top tier investment banks and trading houses.

* Trump, unhappy with latest peace proposal, says Iran “figuring out its leadership”

* UAE leaves OPEC in blow to global oil producers’ group

* US stocks lower on renewed AI growth worries ahead of megacap tech earnings

* Gold and silver drop as Middle East tensions keep USD, oil high

FX: USD rose above the 100- and 200-day SMAs at 98.48/53 as the geopolitical heat turned up as President Trump was reportedly ‘not satisfied’ with Tehran’s proposal to reopen the Strait of Hormuz. Rising oil price have ensued, but the dollar is likely not benefitting as much as it should be due to resilient US stocks and month-end flows given relative US equity outperformance. Watch US tech earnings today and Thursday as they could change the narrative and potentially impact FX.

EUR bounced off its 200-day SMA at 1.1675 with the daily RSI just above 50. Initial disappointment at US-Iran talks turned slightly through the day. Market expectations for Thursday’s ECB meeting have grown more hawkish in the past week due to higher oil prices. But they increase the risk that the hawkish bar may not be met by a still relatively cautious ECB. President Lagarde’s press conference will be key for clues around the timing of any policy action and how likely a pre-summer hike is. She certainly will not want a repeat of the too early hike error another French ECB chief, J-C Trichet, made just before the EZ crisis in 2011.

GBP slid to the 100-day SMA at 1.3459 before bouncing. Sterling was mid-pack among its peers with much speculation around PM Starmer’s position and leadership. A change at no. 10 has big potential implications for fiscal policy given that self-imposed rules could be broken with a more left-wing PM. Near-term, focus is on Thursday’s BoE meeting with almost 60bps of rate hikes priced in for 2026 and 16bps for the June meeting. Governor Bailey previously pushed back against market pricing in tightening while most officials likely want to see more data before action.

JPY wasan outperformer versus its peers after a hawkish hold by the BoJ. The 6-3 vote marked the most significant divide seen during Governor Ueda’s tenure, pointing to increased momentum for policy normalisation. The new outlook report suggests that the energy crunch affects inflation more than GDP growth. The board members’ forecasts also indicate that they are more worried about faster inflation than the risks around activity. That said, there was little on timing of the next rate hike, though money markets assign a high chance of a move in June at the next meeting.

US stocks: The S&P 500 lost 0.49% to close at 7,139, the Nasdaq was 1.01% lower at 27,029 and the Dow Jones settled down by 0.05% at 49,141. The SOX, the semiconductor index which has surged over 40% in 2026, turned sharply lower dragging on the Nasdaq and tech more broadly. Nvidia, Broadcom, AMD and Oracle all declined. Spotify plunged 12.4% after its met guidance but its operating income guidance disappointed. Regarding earning, we’ve had 149 S&P 500 companies report Q1 results, equivalent to around 30% of the index. Top-line growth is currently 9.2%, while bottom-line growth is 15.5%. This week’s earnings matter because roughly 43% of the S&P 500 is reporting and for big tech, the market is no longer rewarding AI ambition alone. It now wants evidence that spending is still producing durable growth, stronger earnings, and clearer returns on investment. The four hyperscalers alone are expected to spend about $645 billion in 2026, up roughly 56% from a year earlier.

Asian stocks: Futures are mixed. APAC stocks traded softer amid downbeat news around Trump unlikely to agree to Iran’s proposal. The ASX 200 dipped as utilities underperformed though energy held up supported by higher crude. The Nikkei 225 came off Monday’s record high above 60,000 as the hawkish BoJ and rate hikes saw sellers emerge. The Hang Seng and Shanghai Composite followed the regional muted mood.

Gold rolled over as the dollar and Treasury yields moved higher. Rising oil prices have put the focus back on crude-induced inflationary pressures, which makes non-yielding bullion less attractive.

Day Ahead – Fed & Bank of Canada meetings

Consensus expect the Fed to leave rates unchanged at 3.50-3.75% at this April meeting. The impact of the ongoing Middle East conflict has lifted energy prices, weighed on consumer confidence, and effectively removed market pricing for near-term rate cuts. The inflation backdrop has worsened, with upward revisions to PCE inflation forecasts, the Fed’s preferred gauge, through year-end. Some of the more dovish Fed officials have acknowledged that inflation remains too high, reducing the urgency for policy easing. However, medium-term and long-term inflation expectations remain relatively anchored so far, with energy pressures unlikely at this stage to feed meaningfully into core inflation. The FOMC will not release updated economic projections at this meeting with the next SEP due in June. At the March meeting, officials pencilled in just one rate cut before year-end. On the leadership side, nominee Kevin Warsh appeared before the Senate this week and called for “regime change” at the Fed, a topic outgoing Chair Powell is likely to face questions on at his post-meeting press conference.

The Bank of Canada is expected to keep rates on hold amid ongoing uncertainty over trade with the US and the war in the Middle East which favour a patient approach to monetary policy. The latest inflation data came in cooler than expected but had little impact, while the labour market has slowed in recent months. Money markets are pricing in roughly 37bps of hikes by year-end, but many expect policy to remain unchanged for the rest of 2026.

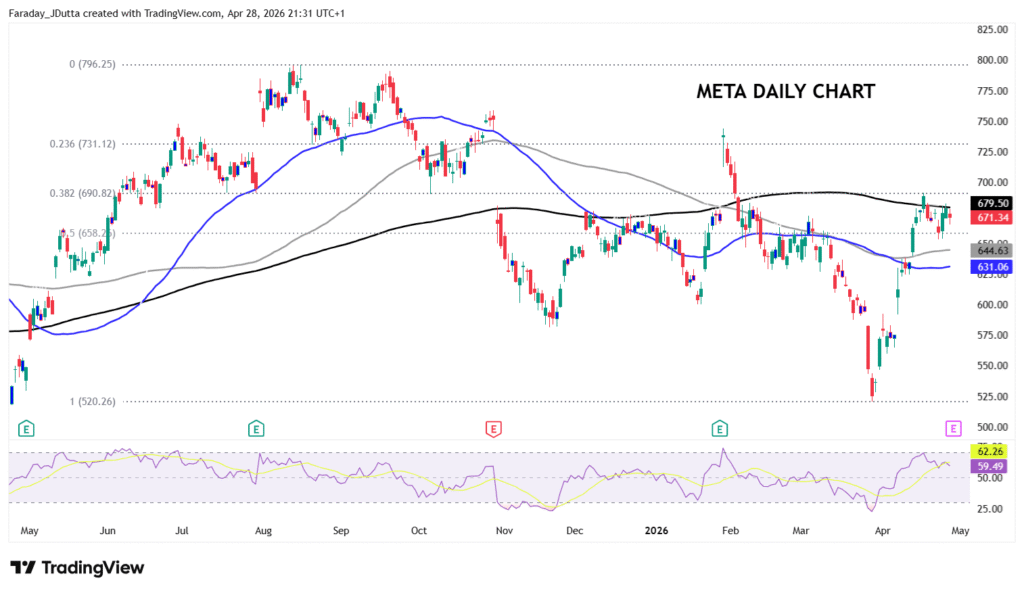

Chart of the Day – Can Meta break above the 200-day SMA?

Meta’s results look like being a test of the ad machine versus the ongoing capex surge. Investors will want to see ad revenue stay hot, while also watching how much Meta plans to spend on AI infrastructure and whether that still leaves room for margin expansion. If ads stay strong and spending looks disciplined, the stock can keep its premium; if capex spikes too hard, growth investors may get nervous fast. Chartwise, prices have consolidated and been trading sideways under the 200-day SMA at $679.49 and two Fibonacci retracement levels from the record high in August to the recent March low at $658.20 and $690.82. Bulls will aim for $731 and the 2026 top, with the 100-day SMA below at $644.59. Options markets see the stock moving +/- 6.9% on the Thursday open.