Taco Tuesday: Trump blinks again after stocks slide, oil pops

Jamie Dutta >

Jamie Dutta >

Jamie Dutta is a Market Analyst for Vantage. He comes with extensive experience as a full-time trader and financial market commentator, having worked as a trader in top tier investment banks and trading houses.

* After markets close, Trump extends ceasefire with Iran until talks conclude

* Vance remain in Washington as uncertainty grows over US-Iran peace talks

* Stocks slip and oil rises as markets awaited negotiation progress

* UnitedHealth jumps on better earnings, outlook and $2bn share buyback

FX: USD climbed up to the 200-day SMA at 98.52 before paring gains on Trump’s TACO. Markets were in ‘wait and see’ mode ahead of the ceasefire deadline and whether any talks in Pakistan between the US and Iran would go ahead. The market had generally taking a ‘half-full’ stance with both sides expected to avoid any major military escalation. Fed Chair appointee Kevin Warsh appeared in front of the Senate Banking Committee. He told lawmakers that central bank policy independence and better decisions are crafted by “steering clear of distractions” and that he is committed to ensuring that rate setting “remains strictly independent”. Retail sales beat estimates as consumers continued to increase spending on non-fuel products.

EUR dipped below the major Fib level (61.8%) of this year’s low to high move at 1.1826 before closing below. Geopolitical developments remain a primary drive. There were disappointing ZEW German business figures while ECB speakers have mostly been leaning mainly towards patience (President Lagarde) or prudence (de Guindos) with very little chance of a rate hike at next week’s ECB meeting.

GBP outperformed many of its peers as cable consolidated recent gains and remained just above 1.35. The latest employment report showed some unexpected job losses, but these were offset by a modest increase in wage growth. Political risks are rising, and PM Starmer’s leadership is being questioned again after a former senior Foreign Office official delivered harsh testimony. The main risk for the GBP relates to the fiscal consequences of possible changes if a more left leaning leader takes the reins. Bond markets would very likely not take this well with yields jumping.

JPY underperformed as the major traded above a prior cycle high at 158.87. Media reports suggested the BoJ intends to deliver a hawkish hold at next week’s meeting, eliminating any lingering expectations of a hike as it assesses the Middle East situation, while keeping the door open to a move in June. The technical picture for the major is neutral and roughly bound between the mid-157s and low 160s, with the 50-day SMA now at 157.62. The longer prices track sideways, typically the bigger the breakout will be.

US stocks: The S&P 500 lost 0.63% to close at 7064, the Nasdaq was 0.42% lower at 26,479 and the Dow Jones settled down by 0.59% at 49,149. Energy was the only sector in the green, with Real Estate, Utilities and Industrials the biggest sector losers. UnitedHealth surged 7% as it beat on earnings, lifted its full year outlook and announced a $2 billion share buyback. Amazon added 0.7% after agreeing to invest up to $25 billion in AI startup Anthropic. Apple lost 2.5% as it announced a CEO transition with Tim Cook’s 15-year run ending with hardware chief John Ternus being handed the reins.

Asian stocks: Futures are mixed. APAC stocks were mixed with uncertainty over Middle East peace talks. The ASX 200 was muted with softness in health, energy and mining. The Nikkei 225 rallied above 59,000 as BoJ was reported to refrain from a rate hike next week. The Hang Seng and Shanghai Composite were steady amid earnings releases and mixed performance in tech.

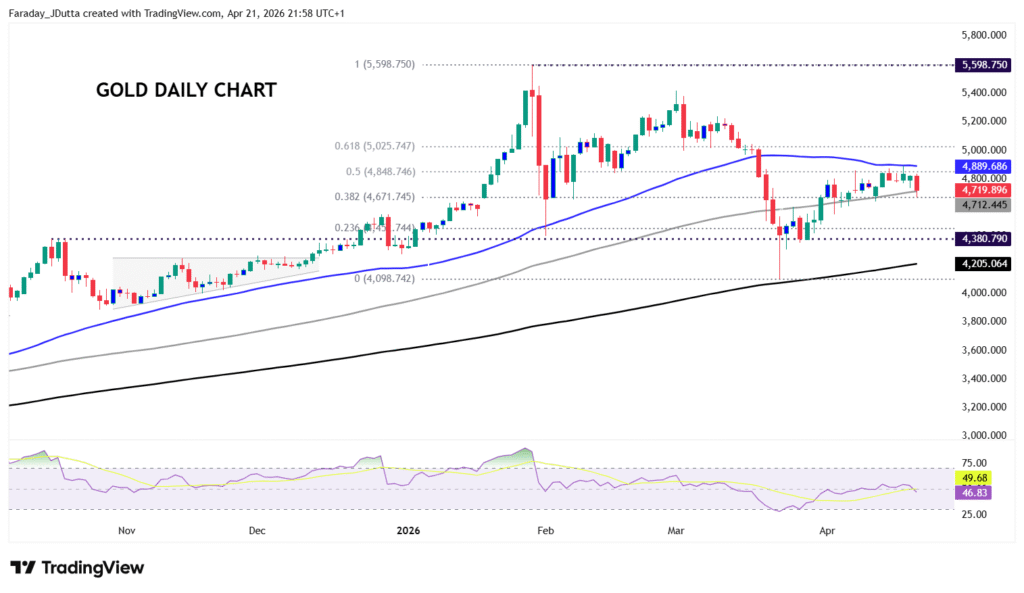

Gold dipped to the bottom of its ascending channel and touched the 100-day SMA at $4,712. The 50-day SMA capped the upside at $4,889.

Day Ahead – UK CPI

Consensus predicts the UK headline inflation rate at 3.3% from 3.0%, boosted by higher petrol and heating oil prices. The core reading, which excludes the volatile energy and food prices, is seen steady at 3.2%. Services inflation, which the BoE watches as a gauge of longer-term inflation pressures, is forecast to tick up one-tenth, after dipping to 4.2% in February, which was the lowest reading since March 2022.

Economists say that quarterly prices cap for household electricity and gas prices means inflation will not rise until July. The increase in March headline inflation is also likely to be much more modest than in the euro area, reflecting the lower weight of fuel in the UK CPI basket (2.7% vs 4% in the euro area). The Bank of England meets next week with no chance of a rate move.

Chart of the Day – Mixed cable chart

Gold fell early in the week amid renewed inflation fears from rising oil and gas prices. Continued disruptions near the Strait of Hormuz are boosting energy markets, increasing inflation expectations and pressuring gold in the short term. Near-term gains may be capped around the 50-day SMA at $4,889; on the flip side the potential for losses seems minimal. Ongoing geopolitical tensions and persistent uncertainty regarding Hormuz should underpin demand for safe-haven assets, or inflation concerns could ease if there is any ceasefire deal if oil drops. Although gold prices have regained part of their losses caused by the Middle East war, they remain lower than pre-conflict levels due to previous liquidity-driven sell-offs. Price action is likely to remain volatile amid shifting expectations around central bank policy, real yields and ongoing geopolitical uncertainty. The 100-day SMA is at $4,712 with a major (38.2%) Fib level of the record high to March spike low at $4,671 and the halfway mark at $4,848.