Oil up, Tech down as stocks reined in by Trump-Tehran tremors

Jamie Dutta >

Jamie Dutta >

Jamie Dutta is a Market Analyst for Vantage. He comes with extensive experience as a full-time trader and financial market commentator, having worked as a trader in top tier investment banks and trading houses.

* Trump aims to seal Iran deal, says truce extension ‘highly unlikely’

* Vance expected to depart US Tuesday for Iran talks in Pakistan

* Oil surges, stocks ease from record highs on tenuous ceasefire

* Strong earnings revisions drive recent stock rally, but concentrated

FX: USD was steady and relatively quiet after Friday’s price action and subsequent weekend news from the Middle East. Even though the Strait of Hormuz is closed again, markets still take the working assumption that both sides will try to avoid an outright new military escalation. That means there is some risk aversion but no panic. The greenback has found support at the midpoint of this year’s low to high move at 98.09. The Fed is in blackout mode ahead of next week’s FOMC meeting, Chair Powell’s last one before he is set to leave office. Today sees Kevin Warsh’s confirmation hearing at the Senate Banking Committee for the role of Fed Chair. He is expected to be dovish on rates, but hawkish on the size of the Fed’s balance sheet

EUR rose and outperformed mildly in a quiet day. Frid. ay saw a rejection of the major Fib level (61.8%) of this year’s low to high move at 1.1826. But prices bounced off the 50% marker at 1.1746. ECB officials will go quiet on Thursday ahead of their meeting next week, with most on message that the ECB is prepared to act and hike rates should it be necessary, but that more time is needed. That means the market has priced out a rate hike next week and now attaches only roughly 50% probability of a June move. PMIs are the major data release on Thursday.

GBP performed similar to most of its peers as cable moved above 1.35. Policy tightening has been reined in ahead of next week’s BoE meeting, with markets currently pricing in one 25bp hike this year. Domestic politics is noisy with the former US ambassador Mandelson scandal reignited and apparent scheming by some senior Labour party officials to topple PM Starmer. Watch this space, as this may take its toll in the months ahead, especially after the May local elections.

JPY onceagainunderperformed as the major continued to trade around a prior cycle high at 158.87. Comments from the BoJ remain relatively hawkish, guiding rate expectations for a June hike which has erased expectations for a rise at next week’s meeting. The technical picture for the major is neutral and roughly bound between the mid-157s and low 160s, with the 50-day SMA now at 157.62.

US stocks: The S&P 500 lost 0.22% to close at 7,110, the Nasdaq was 0.31% lower at 26,590 and the Dow Jones settled down by 0.01% at 49,443. Six sectors were in the green, with Materials, Financials and Real Estate leading the gains. Communication Services, Health and Utilities were the biggest laggards. Marvell said it is in talks with Google to build new AI chips, which comes on the back of last month’s Nvidia announcement backing it with $2bn. The stock is up 74% in 2026 after a 5.8% gain yesterday. Earnings season is cranking up with United Health, GE, RTX, Tesla, IBM, Intel, American Express and Procter & Gamble all reporting this week. So far, 8% of S&P 500 companies have reported, with top‑line growth running near 9%, well above the historical average, which translates into double‑digit earnings growth. Cyclicals results are thriving and expected to approach 25% y/y, with surprises already meaningfully positive.

Asian stocks: Futures are mixed. APAC stocks were mostly higher from the record Wall Street closes but weekend headlines capping much upside. The ASX 200 was little changed with financials muted. The Nikkei 225 rallied up to 59,000 as BoJ rate hike bets were unbound. The Hang Seng and Shanghai Composite were higher amid earnings updates though more gains were capped by few catalysts.

Gold and silver declined as the renewed disruption in Hormuz stoked inflation concerns tied to an energy supply shock and cast further doubt over efforts to end the conflict. Bullion slipped below $4,800 but closed off its worst levels.

Day Ahead – Geopolitics, UK Jobs, US Retail Sales,

US media suggest Vice President Vance, Witkoff and Kushner could meet with the Iranian delegation as soon as today or Wednesday, while Iranian reports indicate no decision has yet been made. President Trump also signalled he is unlikely to extend the ceasefire or remove the US blockade without a deal, while Iran has pushed for the blockade to be lifted before negotiations resume, underscoring the fluid nature of the situation.

The UK labour market was fragile before the Middle East shock and that is expected to continue the longer the conflict continues. Unemployment is expected to stay steady at 5.2% but a further slowdown in public-sector pay growth should drag down average weekly earnings to 3.4%. Looking ahead, the BoE’s Decision Maker’s Panel suggests firms see limited second‐round effects, with year‐ahead wage expectations easing to 3.5% in the March survey, even as year ahead inflation expectations rose to 3.5%.

US March retail sales will be a first look at ‘hard data’ on consumption for that month after the start of the Middle East conflict. Higher gasoline prices will lift the headline figure so focus should be on the core ‘control’ metric that strips out gasoline and autos among other components. Consensus expects a slowdown in growth from 0.5% m/m in February to 0.2%. The K-shaped economy will likely show up, with higher income households continuing to outspend lower income budgets. Tax refunds should support spending going forward.

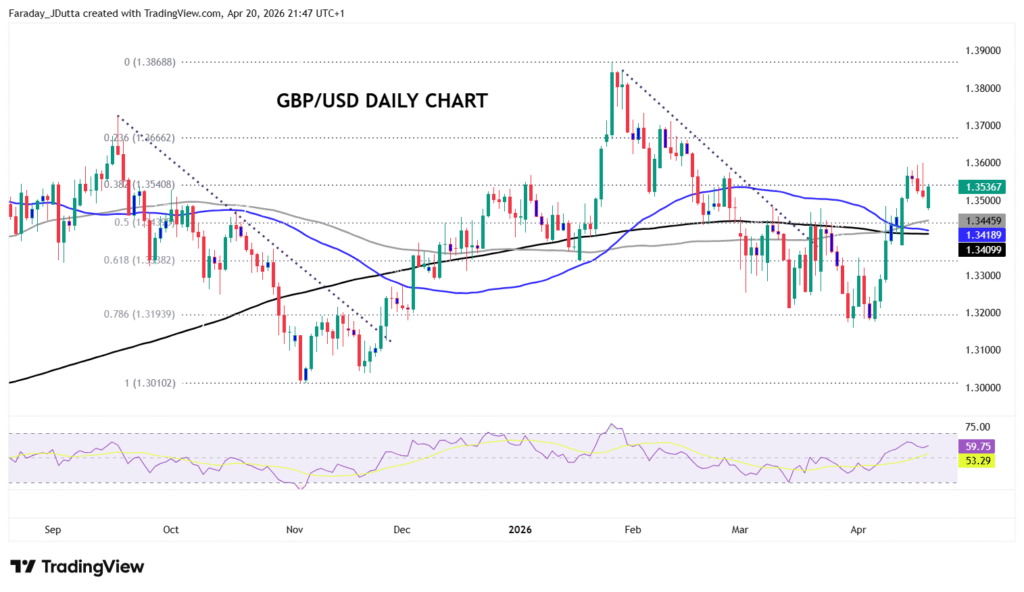

Chart of the Day – Mixed cable chart

GBP has been performing reasonably well in recent weeks, despite the market removing a lot of the expected Bank of England tightening this year. The market still prices one quarter point rate hike this year, after roughly four moves at one point being predicted by traders at the peak of the Middle East tensions. It’s UK data dump week with jobs, CPI and retail sales figures all released over the next few days. The RSI has flattened out in modestly bullish territory with a pair of offsetting doji candles that also hint to a mixed chart. Potential support sits in the mid/ lower-1.34s around the 50- and 200-day SMA’s. Last week’s high resides at 1.3599.