You are visiting the international Vantage Markets website, distinct from the website operated by Vantage Global Prime LLP ( www.vantagemarkets.co.uk ) which is regulated by the Financial Conduct Authority ("FCA").

This website is managed by Vantage Markets' international entities, and it's important to emphasise that they are not subject to regulation by the FCA in the UK. Therefore, you must understand that you will not have the FCA’s protection when investing through this website – for example:

You will not be guaranteed Negative Balance Protection

You will not be protected by FCA’s leverage restrictions

You will not have the right to settle disputes via the Financial Ombudsman Service (FOS)

You will not be protected by Financial Services Compensation Scheme (FSCS)

Any monies deposited will not be afforded the protection required under the FCA Client Assets Sourcebook. The level of protection for your funds will be determined by the regulations of the relevant local regulator.

If you would like to proceed and visit this website, you acknowledge and confirm the following:

1.The website is owned by Vantage Markets' international entities and not by Vantage Global Prime LLP, which is regulated by the FCA.

2.Vantage Global Limited, or any of the Vantage Markets international entities, are neither based in the UK nor licensed by the FCA.

3.You are accessing the website at your own initiative and have not been solicited by Vantage Global Limited in any way.

4.Investing through this website does not grant you the protections provided by the FCA.

5.Should you choose to invest through this website or with any of the international Vantage Markets entities, you will be subject to the rules and regulations of the relevant international regulatory authorities, not the FCA.

Vantage wants to make it clear that we are duly licensed and authorised to offer the services and financial derivative products listed on our website. Individuals accessing this website and registering a trading account do so entirely of their own volition and without prior solicitation.

By confirming your decision to proceed with entering the website, you hereby affirm that this decision was solely initiated by you, and no solicitation has been made by any Vantage entity.

By providing your email and proceeding to create an account on this website, you acknowledge that you will be opening an account with Vantage Global Limited, regulated by the Vanuatu Financial Services Commission (VFSC), and not the UK Financial Conduct Authority (FCA).

Our website and services are not available to, and are not intended for, individuals who are citizens or residents of the United States, or entities incorporated in or conducting business within the United States.

If this does not apply to you and you believe you have received this message in error, please contact us at [email protected] for further assistance.

If you fall into any of the above categories, please exit the site.

Important Information

Thank you for visiting the Vantage Markets website. Please note that this website is intended for individuals residing in jurisdictions where accessing it is permitted by Vantage and its affiliated entities do not operate in your home jurisdiction.

By clicking 'I CONFIRM MY INTENTION TO PROCEED AND ENTER THIS WEBSITE', you confirm that you are entering this website solely based on your initiative and not as a result of any specific marketing outreach. You wish to obtain information from this website based on reverse solicitation principles, in accordance with the applicable laws of your home jurisdiction.

* Stocks mixed as defensives outperformovervalued tech

* Dollar slides on signs of US labour market weakness

* GBP underperforms on soft labour market data and rising BoE rate cut bets

* US shutdown nears end as Senate passes deal, House readies vote

FX: USD dropped sharply after soft weekly ADP employment data showed that employers shed jobs (-11,250) in the four-week period through October 25. The 200-day SMA sits at 100.20. This weak labour market data comes as the government shutdown is about to come to an end, which means we may get a torrent of economic data in the coming days and weeks. Goldman Sachs reckons deferred government resignations could see a 50k drop in the headline October NFP print. There’s around a two in three chance of 25bps Fed rate cut next month.

EUR picked up as it traded around near-term resistance at 1.1591. The 50-day SMA is at 1.1663. The German business ZEW survey data disappointed as ‘structural problems continue to exist’. There was mixed ECB commentary with data dependence and inflation risks now broadly balanced the key takeaways, so nothing new.

GBP lagged its peers after weaker than expected jobs data. Key wage growth matched forecasts but the unemployment rate ticked higher with employment contracting. Cable dropped to the low of the day at 1.3116 before climbing higher through the day, mainly on dollar weakness. BoE rate cut odds turned marginally more dovish, with above a 70% chance of a December 25bps move. The MPC’s Greene noted the report was ‘not great’ and cautioned around a cloudy jobs picture.

JPY initially softenedas the major bumped into resistance around 154.44/48, before the dollar grew weaker through the session. The yen has been under pressure after new PM Takaichi called for the BoJ to go slow on policy normalisation.

US stocks: The S&P 500 gained 0.21%, closing at 6,847. The Nasdaq moved lower by 0.31% to settle at 25,533. The Dow Jones finished at 47,928, up 1.18% on the day. Only technology was in the red with Healthcare, Energy, Consumer Staples, Real Estate and Materials all up by more than 1%. Mag 7 stocks are choppy at the moment as they most fell after a solid rally on Monday, though Apple, Microsoft and Alphabet stayed positive. Nvidia suffered the most after Japan’s Softbank said it sold its entire stake in October, though this was to fund other AI investments. Coreweave shares plunged 16.3% despite revenue more than doubling at the AI data-centre operator. Paramount Skydance jumped over 9.7% as investors cheered the new CEO’s pitch on remaking the storied media house for the streaming era, with further cost cuts and plans to invest $1.5bn next year.

Asian stocks: Futures are mixed. Stocks were muted as there was little positive follow-through from Wall Street’s gains after the optimism around the US government shutdown nearing an end. The ASX 200 saw early gains by gold miners and stocks offset by bigger weakness in tech and financials. Earnings growth by Cba was modest. The Nikkei 225 initially rallied on yen weakness before it gave up gains and turned red. The Hang Seng and Shanghai Composite were lower amid tech selling and a disappointing start to China’s Singles Day shopping sales.

Gold had a mixed day as it kicked off with more buying to a high at $4,148, a two-and half week high. But sellers emerged to see it trade modestly higher on the day.

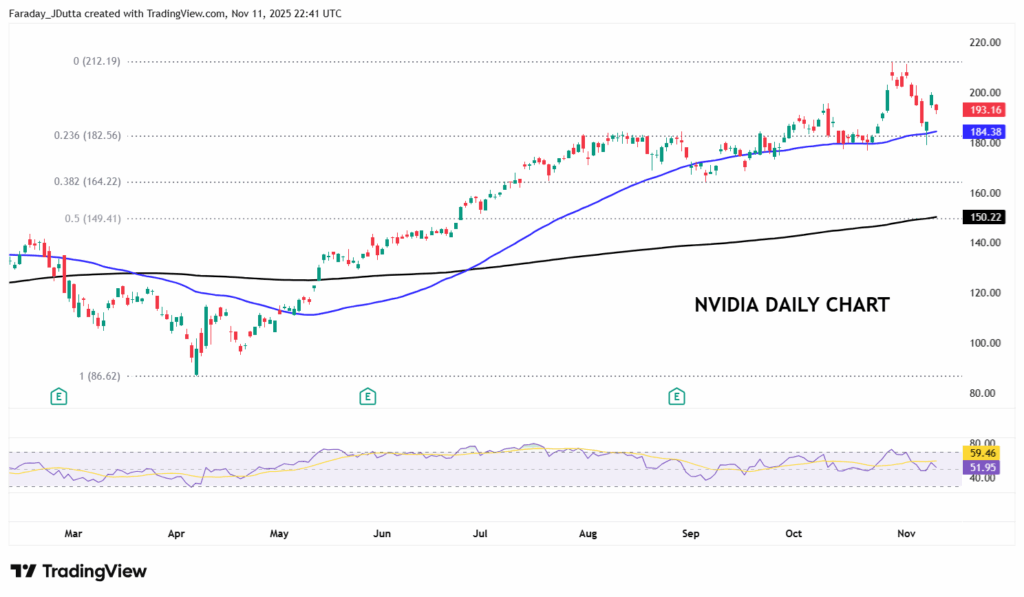

Chart of the Day – Choppy price action in NVDA

We covered the tech-laden Nasdaq yesterday, and where Nvidia goes, so do the broader indices. This is because a $5 trillion market cap gives you a roughly 7.6% and 13.9% weighting in the S&P 500 and Nasdaq respectively. As concerns ramp up about AI valuations and AI capex, last week saw the world’s biggest stock by market cap suffer its worst week since mid-April, falling over 7%. Prices touched the 50-day SMA on Friday but bounced back strongly and on Monday. That is well watched momentmu indicator is currently at $184.80. That level sits just above a minor Fib level (23.6%) of the April rally to record high at the end of last month at $182.56, reinforcing it as a strong support zone. The record top is at $212.19 with their earnings report due next Wednesday after the US market close. Guidance is currently pointing to $54bn in revenue and strong data growth given by Blackwell architecture. Needless to say, this is a big risk event for NVDA, AI and the wider market.

Written on November 11, 2025 at 10:41 pm, by jamie

Comments Off on Two-way trade in stocks, USD lower on soft jobs data

Markets should be expected to offer fresh volatility this week. After the limited momentum during last week’s trading potential new directions might be seen. The Dollar initially geared up some momentum but, in the end, failed to rise. Most currency pairs hence ended the week with Dollar weakness and the trend might now elevate again. Worth noting, though, that the AUD remains subdued and might indicate that the risk sentiment continues to be weak. Stock markets might fall and also cryptos might remain shaky moving forward.

The economic calendar only reveals limited news events this week. Employment data out of Australia and the United Kingdom might move markets while the latter also offers more information with the release of the gross domestic product.

Important events this week:

UK gross domestic product: Despite being a backward-looking indicator the Pound might also face fresh volatility with the release of the GDP report. The economy in the UK has been shrinking recently and a decline towards a growth figure of 0.0% on a monthly basis shows the current trend. Last week the Bank of England did not act leaving the interest rate at 4.0% as the pressure of inflation still looms.

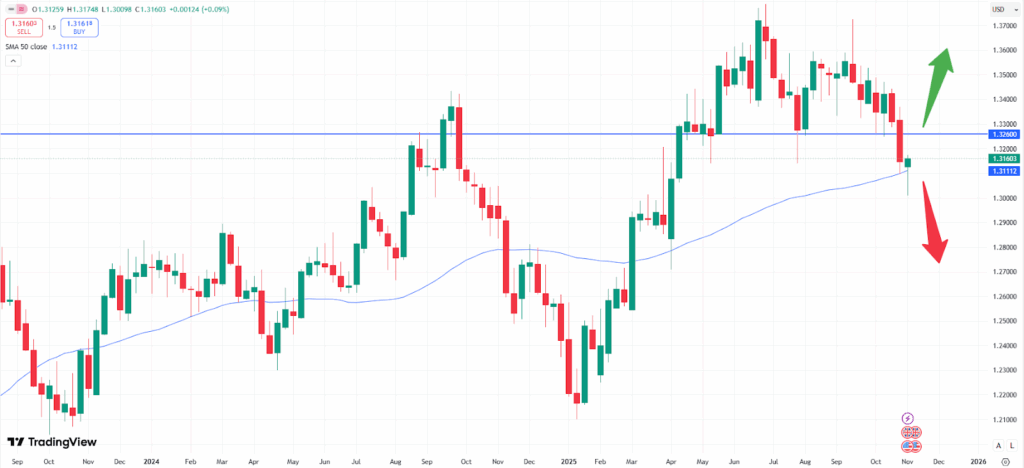

GBPUSD weekly chart

Yet, the Pound has been able to defend the recent slide in prices. Based on the weekly chart the GBPUSD currency pair has stabilized right on top of the 50- moving average support zone. A potential positive release of the news might hence help the Pound to rise against other currencies. A potential rise might be found towards the technical resistance zone at 1.3260, where the bearish trend might kick- in again causing the price to potentially fade again further.

US CPI and PPI data: The longest shutdown in US history might soon show negative impact in markets. As important support for the economy as well as the population is absent in parts negative headlines might soon emerge. Stock markets also offer a slight preview here with prices currently falling. Consumer price data as well as producer prices are due to be released on Thursday and Friday respectively but are being likely delayed again.

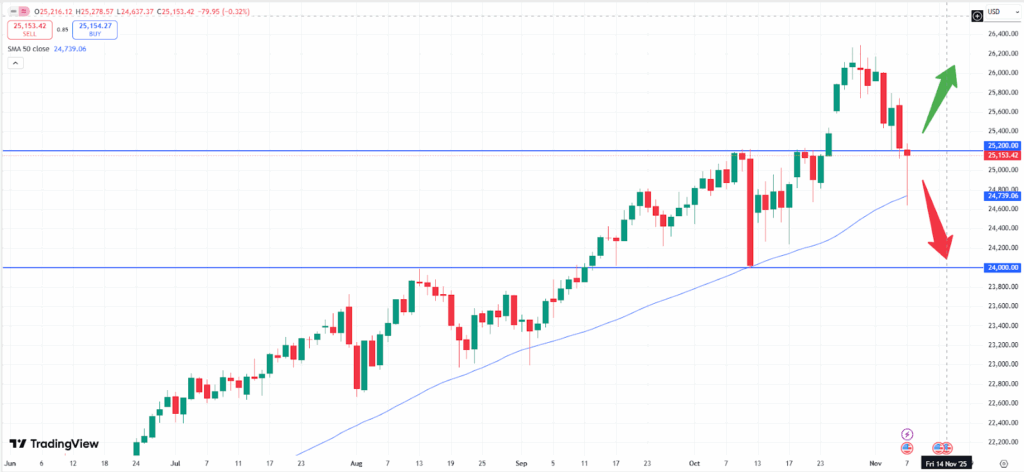

NASDAQ daily chart

The NAS100 index shows that the market retraced last week. Traders should now pay attention to the important support zone of 25.200. A clear break of this level might indicate that the market will start to correct further. The market might then try another attempt towards the 24.000 price range.

On the other hand, the market might start to resume upside momentum again at the 25.000 level, as the zone has been tested a few times in recent weeks. If prices stop falling at that level the upside might be resumed as well. Strong momentum might then be found above the level of 26.000. A new all- time- high might then emerge.

Written on November 11, 2025 at 5:39 am, by jessie

Comments Off on Weekly Outlook | New Directions After Sideways Price Action

* Wall Street rallies on US shutdown optimism, tech rebounds

* Gold climbs to two-week highs as soft data cements rate cut bets

* Yen, CHF lower as safe haven bid recedes, AUD and CAD outperform

* Bessent says Trump’s $2,000 dividend may come via tax cuts

FX: USD was very mildly bid with the dollar relatively quiet on the government shutdown end approaching. High-beta risk currencies may benefit more than the greenback. The 200-day SMA at 100.25 has also got some attention as resistance, along with last week’s weak jobs and consumer sentiment figures. While no (economic) news has been good for the dollar, government re-opening could see more cautious trade, with the slow release of economic data shaping the Fed’s policy into year-end.

EUR paused after three straight days of gains closed last week. Increased Fed rate cut expectations had helped the euro. There’s little eurozone data this week. Near term resistance is at 1.1591 and then the 50-day SMA at 1.1664.

GBP was mid-pack among the majors, with now a four-day rebound from multi-month lows. There’s been a mild rise in UK-US yield spreads which have helped sterling, even though the odds of a BoE December rate cut are firm. Jobs data is released today.

JPY was the major laggard on upbeat risk sentiment, though Treasury yields didn’t respond positively. Initial resistance sits around 154.44/48. New PM Takaichi reaffirmed her comments about central bank independence. BoJ officials also leaned mildly hawkish as the ‘fog surrounding Japan’s economic outlook has begun to clear, compared with July.’

US stocks: The S&P 500 gained 1.54%, closing at 6,832. The Nasdaq moved higher by 2.2% to settle at 25,612. The Dow Jones finished at 47,369, up 0.81% on the day. All sectors were green apart from three with Tech, Communication Services and Consumer Discretionary up from 2.69% to 1.49%. Those mega-cap sectors outperformed with all Mag-7 names in positive territory. Consumer Staples was one of few sectors in red and saw a lack of demand due to its risk-off defensive characteristics. Nvidia surged 5.8% and Palantir added 8.8% after progress in Washington to end the 40-day and longest government shutdown. ‘Buy the dip’ has once again lifted tech and AI stocks after both the S&P 500 and the Nasdaq bounced off their 50-day SMAs as support. Eli Lilly rose 4.6% to a record high

Asian stocks: Futures are positive. Stocks traded higher after hopes of the US government shutdown ending sparked optimism. The ASX 200 moved higher led by miners and tech, while disappointing ANZ figures didn’t dent financials. The Nikkei 225 rallied on the weaker yen and earnings. The Hang Seng and Shanghai Composite were both bid on improved US-China trade relations though inflation data printed hotter than expected.

Gold surged over 2.8% as Treasury yields fell though the dollar steadied. Markets weighed signs of economic weakness versus the end of the government shutdown. Attention may get drawn to the poor US fiscal outlook after President Trump offered up $2,000 tariff dividends to low-income families.

Day Ahead – UK Jobs

Jobs data, and specifically wage growth, has been a key metric for the BoE as it feeds into inflation figures. The headline earnings metric is forecast to remain at 5.0% and the ex-wage figure is likely to moderate to one-tenth to 4.6%. September’s unemployment rate is expected to tick up to one-tenth to 4.9%, with the three-month number predicted to cool to around 4.3%, somewhat lower than the BoE’s 4.7% forecast.

The series comes after last week’s November BoE meeting and the and the big focus on inflation. Wage data could provide some early comfort to Governor Bailey, the swing voter on the heavily divided MPC, which saw a closer than expected 5-4 vote to keep rates on hold last week. Overall, the data will add some colour to the underlying inflation picture, but markets are primarily waiting for the next two CPI prints on November 19 and December 17, and the November 26 Budget before the December BoE rate decision. There’s a near 70% chance of a 25bps rate cut at the final meeting of the year.

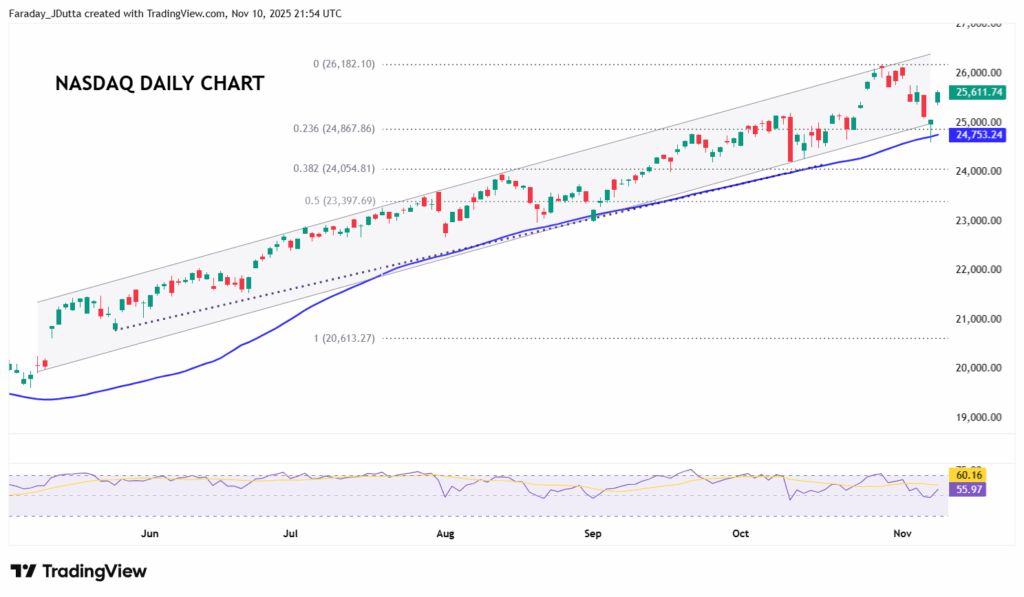

Chart of the Day – Nasdaq back into bull channel

The tech-heavy Nasdaq index suffered last week, falling over 3% in its worst week since April. Investors got worried about sky-high valuations with the combined market value of 8 of the most valuable AI-related stocks – including Nviida, Meta and Palantir – losing around $800bn. Concerns over AI-related capex have risen, with Meta, Alphabet and Amazon reporting over $110bn of AI investments in the third quarter, as they are increasingly debt-financed. But the end of the US government shutdown has seen investors buy the dip after prices fell out of the long-term ascending channel. The index also bounced off its 50-day SMA at 24,748. The recent record high at 26,182. A seasonal melt-up could still be on which we wrote about in a previous Week Ahead.