You are visiting the international Vantage Markets website, distinct from the website operated by Vantage Global Prime LLP ( www.vantagemarkets.co.uk ) which is regulated by the Financial Conduct Authority ("FCA").

This website is managed by Vantage Markets' international entities, and it's important to emphasise that they are not subject to regulation by the FCA in the UK. Therefore, you must understand that you will not have the FCA’s protection when investing through this website – for example:

You will not be guaranteed Negative Balance Protection

You will not be protected by FCA’s leverage restrictions

You will not have the right to settle disputes via the Financial Ombudsman Service (FOS)

You will not be protected by Financial Services Compensation Scheme (FSCS)

Any monies deposited will not be afforded the protection required under the FCA Client Assets Sourcebook. The level of protection for your funds will be determined by the regulations of the relevant local regulator.

If you would like to proceed and visit this website, you acknowledge and confirm the following:

1.The website is owned by Vantage Markets' international entities and not by Vantage Global Prime LLP, which is regulated by the FCA.

2.Vantage Global Limited, or any of the Vantage Markets international entities, are neither based in the UK nor licensed by the FCA.

3.You are accessing the website at your own initiative and have not been solicited by Vantage Global Limited in any way.

4.Investing through this website does not grant you the protections provided by the FCA.

5.Should you choose to invest through this website or with any of the international Vantage Markets entities, you will be subject to the rules and regulations of the relevant international regulatory authorities, not the FCA.

Vantage wants to make it clear that we are duly licensed and authorised to offer the services and financial derivative products listed on our website. Individuals accessing this website and registering a trading account do so entirely of their own volition and without prior solicitation.

By confirming your decision to proceed with entering the website, you hereby affirm that this decision was solely initiated by you, and no solicitation has been made by any Vantage entity.

By providing your email and proceeding to create an account on this website, you acknowledge that you will be opening an account with Vantage Global Limited, regulated by the Vanuatu Financial Services Commission (VFSC), and not the UK Financial Conduct Authority (FCA).

Our website and services are not available to, and are not intended for, individuals who are citizens or residents of the United States, or entities incorporated in or conducting business within the United States.

If this does not apply to you and you believe you have received this message in error, please contact us at [email protected] for further assistance.

If you fall into any of the above categories, please exit the site.

Important Information

Thank you for visiting the Vantage Markets website. Please note that this website is intended for individuals residing in jurisdictions where accessing it is permitted by Vantage and its affiliated entities do not operate in your home jurisdiction.

By clicking 'I CONFIRM MY INTENTION TO PROCEED AND ENTER THIS WEBSITE', you confirm that you are entering this website solely based on your initiative and not as a result of any specific marketing outreach. You wish to obtain information from this website based on reverse solicitation principles, in accordance with the applicable laws of your home jurisdiction.

* Wall Street slides again as valuation concerns, rate cut jitters linger

* Gold gains on soft economic data, dollar quiet as yields dip

* Bitcoin falls to a 7-month low below $90k before rebounding modestly

* Baidu Q3 revenue falls 7% as ad slump offsets cloud growth

FX: USD was little changed as the dollar didn’t gain anything from its typical safe haven status amid downbeat risk sentiment. The 200-day SMA capped the upside recently, and that comes in currently at 99.99, above a long-term swing low from 2023 at 99.57. A surprise weekly initial jobless claims release saw a pick up to 232k from 219k, though this was from mid-October so stale. Markets await NVDA results and the delayed NFP data. Odds of a 25bps December Fed rate cut has edged higher to 49%. Cautious Fedspeak last week saw this dip to 44%. Soft US data would see this move materially higher.

EUR fell for a third day but price action was muted. There’s very little new news for the euro. The euro does traditionally enjoy positive December seasonality, for what it’s worth. The euro’s technical signals are neutral with an RSI hovering around the 50-threshold.

GBP was flat and mid pack among the majors as it continues to consolidate around 1.3150. CPI is released today. BoE Governor Bailey highlighted inflation developments at the most recent MPC meeting and he is likely to be the deciding vote ahead in December. See more details below on the CPI. Otherwise, there were media reports that Chancellor Reeves is reportedly considering a last-minute raid on banking profits in the budget. This would be a politically favourable move, but perhaps overshadowed by growth-related implications.

JPY was the major underperformer again as USD/JPY pushed up to a high at 155.73. BoJ Governor Ueda and PM Takaichi had their first bilateral meeting on Tuesday, with Ueda highlighting the central bank’s intention to continue with their process of making gradual adjustments to policy. There’s only currently around a 28% chance of December rate hike. Major resistance sits at 157.50.

US stocks: The S&P 500 lost 0.83%, closing at 6,617. The Nasdaq moved lower by 1.2% Mega-cap sectors Consumer Discretionary and Technology underperformed amid continued concerns regarding AI overvaluation. These worries were heightened on Tuesday, as an investment bank downgraded both Amazon and Microsoft, saying it’s time to take a more cautious stance on AI hyperscalers. Health and Energy were the outperformers, with the latter boosted by strength in crude, albeit not on any specific headline driver. US data painted a sluggish picture of the labour market as well, dampening risk sentiment. iPhone 17 models lifted October smartphone sales in China by 37%, giving Apple a 25% market share for the first time since 2022.

stocks: Futures are mixed. Stocks extended losses with indices taking their lead from Wall Street. The ASX 200 saw tech hit hard and a clear defensive bias. The RBA minutes emphasised data dependence and uncertainty. The Nikkei 225 sold off and lost the 49k level, eventually sinking over 3%. China-Japan relations have been strained recently amid yen weakness. The Hang Seng and Shanghai Composite opened in the red with Hong Kong underperforming the mainland.

Gold found a bid through the day having dipped below $4,000 at the start of the European session. The 10-year Treasury yield fell to the 50-day SMA at 4.08% but then bounced.

Day Ahead – UK CPI, FOMC Minutes

Analysts forecast the headline UK inflation rate to ease to 3.5% from 3.8% due to base effects after the Ofgem adjustment. Core CPI is forecast at 3.4%, one-tenth lower than in August. Services inflation should also cool with softer wage growth. BoE December rate cut odds for a 25bps move stand around 80%. There is one more CPI report before that final meeting of 2025.

The FOMC minutes will see markets alert for clues on the Fed’s policy bias following the ‘hawkish’ cut in October, only the second this year. Focus will be on the heavily divided Fed which had one hawkish and one dovish dissenter, and what was deemed a hawkish Powell press conference. He pushed back against expectations for a December rate cut, stressing data dependence amid the shutdown-related dearth of economic data. Markets see a 46% chance of a 25bps December rate cut.

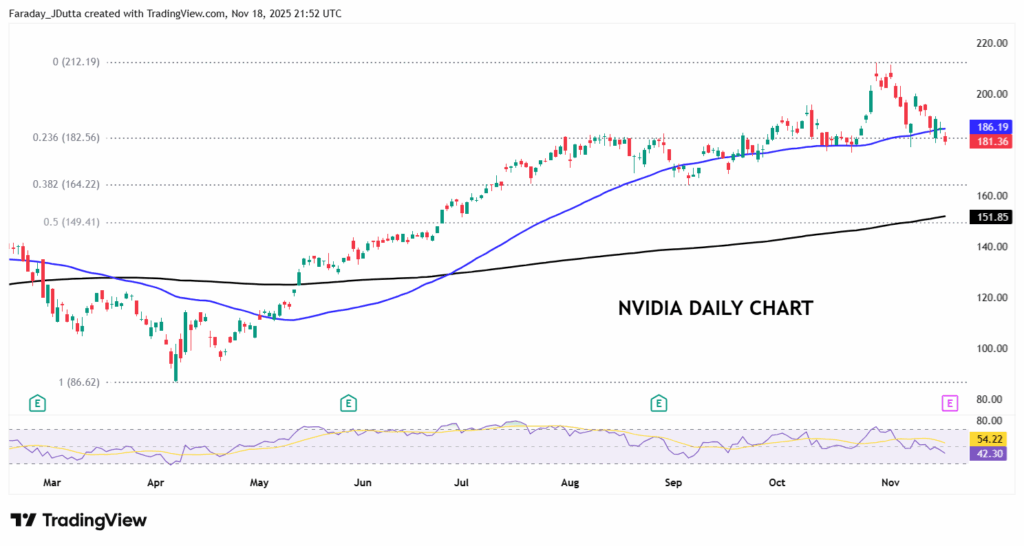

Chart of the Day – Nvidia below 50-day SMA

NVDA is the bellwether and gauge for the stock market (AI) rally. Markets predict NVDA could move 6.5% up or down in the trading session on Thursday, after its earnings release. The stock is up 34% this year. Wall Street analysts expect EPS of $1.23 per share, revenues of $54.7 billion for the quarter and growth rates of 50%++ revenue plus large EPS gains. Investors will be watching any “beat and raise” guidance, especially around next-quarter revenue and shipments of new chips (Blackwell, GB300), and strong demand in the data-centre business, which is the largest driver of growth and margins. Demand from the outside the big four hyperscalers will be a focus. Supply bottlenecks, margins and China exposure will also be analysed, as any signs of risk will matter for investor sentiment. The record high sits at $212.19, the 50-day SMA at $186.24 and a minor Fib of the April to November rally at $182.56. The next retracement (38.2%) is at $164.22.

Please be advised that EU stock Takeaway.com NV (TKWY) on Vantage’s platforms will be removed on 17 November 2025 as it is expected to be delisted from exchange.

If you have any questions or require assistance, please do not hesitate to contact [email protected].

Written on November 17, 2025 at 9:37 am, by manroulau

Comments Off on Delisting and Closing Position of EU Stock TKWY

A super interesting week lies ahead after a relatively tumultuous few days in which stocks saw flows shift from supportive to destructive. We had been hinting at this for a while, with stretched AI valuations and the recent hawkish Fed rate cut all primed to grab centre stage at some point. Of course, timing these things is what we all try and do best; after all, we are here to tell you about significant themes in a timely fashion, and when they might impact the market and price action.

The ‘elevator down’ dynamics were in play in the latter part of last week. This describes the tendency for the stock market to experience sharp, rapid declines (‘elevator down’) after a period of gradual growth (‘stairs up’). Investor psychology plays a big part in this as relative fear can cause panic selling amid 24/7 news coverage about “Wall Street tumbling”. Market dynamics are also key as huge trading algos amplify the drops. And yet the benchmark S&P 500 is actually still less than 4% from its record high while the tech-laden Nasdaq is around 5.7% off its all-time top.

Do we get a seasonal Santa rally? A healthy correction of frothy markets is historically a good thing over the long term. Much will depend on Nvidia’s results which will be published after the US closing bell on Wednesday. Focus will be on commentary around demand and spending trends. Also of note will be some of the biggest US retailer earnings reports, like Walmart and Home Depot, which will be published through the week.

The dearth of US data had left FX markets volatility muted but this will pick up this week with the release (finally!) of the US September NFP report (and NVDA’s results). We note open interest on bullish Treasury options increased significantly last week, suggesting the prevailing call is for soft US data which will prompt dovish Fed repricing. But markets have shifted in recent days on more hawkish Fedspeak, with traders now seeing only a 45% chance of a 25bp December Fed rate cut from near double this less than a month ago. Again, we’ll be watching both the S&P 500 index and Nasdaq’s 50-day SMAs as support/resistance. We haven’t seen three straight weeks of losses in the Nasdaq since March.

In Brief: Major data releases of the week

Monday, 17 November 2025

Canada CPI: The Bank of Canada expects inflation to ease as energy prices fall. But base effects may see price pressures pick up in the short-term, early in the new year.

Wednesday, 19 November 2025

UK CPI: Analysts forecast the headline rate to ease to 3.6% from 3.8% due to base effects after the Ofgem adjustment. Services inflation should also cool with softer wage growth. BoE December rate cut odds for a 25bps move stand around 80%.

FOMC Minutes: Markets will focus on the heavily divided Fed which had one hawkish and one dovish dissenter, after what was deemed a hawkish Powell press conference. Markets see a 25bps December rate cut as a coin toss.

Nvidia Earnings: The AI boom bellwether reports after the US closing bell. Consensus forecast EPS of $1.25 on revenues of $55.1bn. Options markets see a +/- 6.4% implied one-day move post-results. Nvidia carries an 8% weight in the S&P 500 and a roughly 10% weight in the widely followed Nasdaq 100, so as we always say, where NVDA goes, so too the market.

Thursday, 20 November 2025

Japan CPI: October nationwide inflation is expected to accelerate driven by broad-based goods and services price gains. Tokyo CPI has been hot in recent months, and this could cause the odds of a December BoJ hike to increase, which currently sit around 32%.

US Non-Farm Payrolls: Consensus estimates of this September data are vague, and the report is somewhat dated. Job estimates come in around 45k with an unemployment rate remaining steady at 4.3%. Alternative labour market data have painted a mixed picture with growth sluggish but not falling apart.

Friday, 21 November 2025

Global PMIs: Services should likely bolster the composite print in the eurozone, though there’s recently been a series of disappointing hard data. UK PMIs may be clouded by budget uncertainty again, after worse than expected metrics in September.

* Wall Street lower ahead of Nvidia results and data deluge

* Dollar marginally firmer as markets await return of data

* Bitcoin erases all 2025 gains after $600bn fall

* Markets see a near 60% chance of the Fed sitting on their hands in December

FX: USD was firmer in pivotal week for the greenback. The government reopening means we get data releases, with September NFP taking centre stage. That said, it is a few months old but it will give us a steer towards how the labour market softness is unfolding. Odds for a December Fed rate cut have dipped below 50:50 to 40% for a move. That was double that less than one month ago. The Dollar Index has found support on the near-term upward trendline from the late September low. The 200-day SMA capped the upside recently, and that comes in currently at 100.03, above a long-term swing low from 2023 at 99.57.

EUR moved lower for a second day in a row even though interest rate differentials are nearing three-month highs. The dollar is the main driver ahead of the FOMC minutes and NFP release later this week. The ECB is in neutral mode and a ‘happy place’ regarding policy. The main data point this week are Friday’s PMI figures.

GBP outperformed as cable printed an inside day doji denoting some uncertainty. That isn’t surprising considering the huge amount of speculation and headlines we have seen pre-November 26 Budget. Sterling is getting some support as rate differentials have narrowed in recent days. Data comes thick and fast this week with CPI on Wednesday, and retail sales and PMIs on Friday. There’s currently around a 79% chance of a 25bps BoE rate cut next month.

JPY was the major underperformer as USD/JPY broke to the upside above 155. Better than expected Japan GDP was no help as investors wait for CPI published on Friday to determine if BoJ rate hike odds should increase from around 30% at present. Likely jawboning against the speed of the currency move may come from MoF officials.

CAD saw slight two-way trade on the latest inflation data. It was mixed as headline inflation Y/Y eased but was slightly above consensus. Core inflation picked up in October partially due to one-off factors.

US stocks: The S&P 500 lost 0.91%, closing at 6,672. The Nasdaq moved lower by 0.83% to settle at 24,800. The Dow Jones finished at 46,590, down 1.18% on the day. All but two sectors were negative with only Communication Services and Utilities in the green. Financials, Energy, Materials and Tech lagged, all down by more than 1.4%. Big Tech was broadly lower with Alphabet closing 3.1% higher on the back of Berkshire Hathaway of Warren Buffett fame, buying up nearly $5bn in stock in Q3. This was likely one of the last major investments with the Sage of Omaha at the helm and is a rare foray into AI. Apple is said to be speeding up the CEO succession planning as Tim Cook could step down as early as next year. The stock closed 1.8% lower. High valuation concerns continue to spook investors with all three major stock indices finishing below their 50-day SMAs.

Asian stocks: Futures are mixed. Stocks traded mostly lower after weekend news that President Trump won’t be rolling back any tariffs. The ASX 200 was muted again with tech and energy outperforming and telecoms and health lagging. The Nikkei 225 was choppy as it dipped under 50k before paring losses. GDP contracted for the first time in six quarters. Tensions between China and Japan also saw travel related names hit as Beijing warned citizens not to travel and study in Japan. The Hang Seng and Shanghai Composite were modestly lower on mixed trade news and Bessent optimism that a rare earths deal will be reached by Thanksgiving.

Gold fell for a third straight day as Fed rate cut bets diminished for the December FOMC meeting. There’s now only a 40% chance of a 25bps move next month, versus over 90% one month ago.

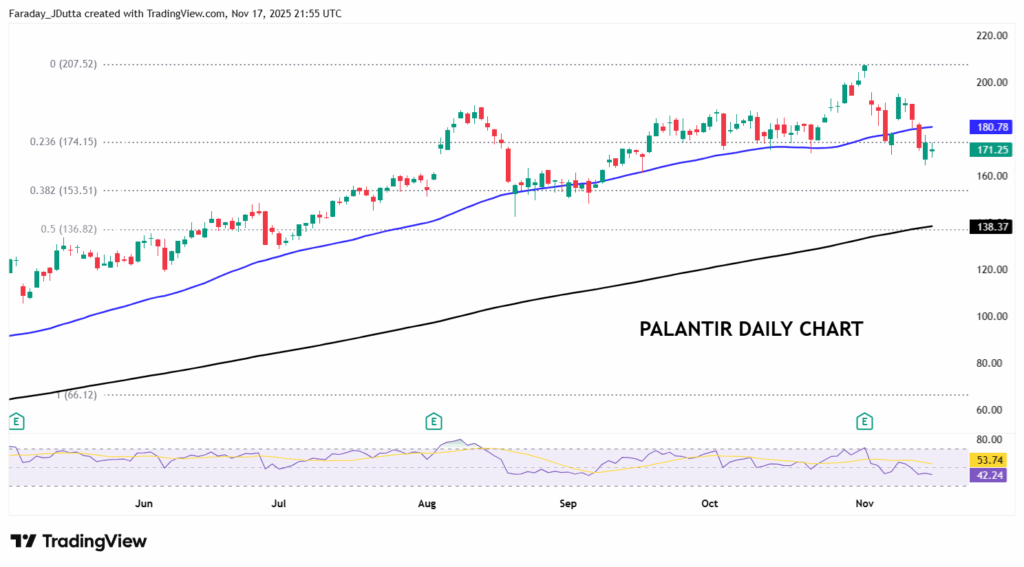

Chart of the Day – Palantir pulls back

Palantir slid 7% after its earnings at the start of the month, though that barely dented gains of more than 125% year-to-date. Enterprise AI names priced for perfection and stretched valuations have come under big pressure recently as investors now focus on ‘jam today’, and not tomorrow. The recent record high just before the release of its results was $207.52. Prices fell but found support around the minor Fib level (23.6%) of the April to November rally at $174.15. The 50-day SMA sits at $180.78. The major Fib level below (38.2%) resides at $153.51.