Risk-on as oil tumbles on ‘fragile’ US/Iran ceasefire

Jamie Dutta >

Jamie Dutta >

Jamie Dutta is a Market Analyst for Vantage. He comes with extensive experience as a full-time trader and financial market commentator, having worked as a trader in top tier investment banks and trading houses.

* Two-week ceasefire agreement clouded by confusion and contradictions

* Risk sentiment boosted by ceasefire and Hormuz Strait reopening optimism

* Crude plunges, dollar falls as market reverses war risk premium

* Stocks sharply higher, Dow posts best day since April 2025

FX: USD gapped lower and fell sharply though closed off its lows. The index also broke below trend support drawn off the late January low. If we get a further decline in broader market volatility with the VIX, Wall Street’s fear gauge, dropping below the 20 level, that should signal more sustained pressure on the buck. Prices touched the 100-day SMA at 98.64 and a long-term Fib level at 98.70. There is a support zone of two other SMAs as well around 98.48/64. More dollar losses should follow if the area does not hold. That depends on if the 2-week ceasefire holds but it seems there is much doubt as to that happening, with tough compromises likely needed to agree to the 10/12-point plan.

EUR was a laggard among its peers as it initially rose above the 50,100 and 200-day SMAs to a one-month high around 1.1672/85 at the start of the US session, before pulling back. Ceasefire developments mean there is less pressure on the ECB to lift rates for now, though the situation is still fragile. There are still around 50bps of hikes priced in for 2026.

GBP peaked at a near 6-week high at 1.3484 before pulling back below long-term SMAs. Importantly, cable closed just below the 200-day SMA at 1.3414. Broader market sentiment is dominating.

JPY strengthened as the dollar dipped, with the major falling to a low at 157.88. Falling oil and energy prices dramatically improve Japan’s terms of trade and should give decent reprieve to the yen if the ceasefire holds. Important labour cash earnings data came in stronger than expected, delivering added support for a continued policy normalisation and BoJ tightening.

NZD outperformed, helped by the positive risk mood after the Middle East optimism, plus remarks in the RBNZ’s post-meeting press conference. Governor Breman said the MPC discussed the possibility of raising rates in April and May meetings, and the “frequency of rate hikes could be every meeting or every second meeting”. Prices hit the 200-day SMA at 0.5849 and pulled back.

US stocks: The S&P 500 added 2.52% to close at 6,783, the Nasdaq was 2.9% higher at 24,903 and the Dow Jones settled higher by 2.85% at 47,911. The Nasdaq and Dow Jones moved above their 200-day SMAs. Both hit their 50-day and 100-day SMAs. Industrials, Communication Services and Materials all surged by more than 3%. All sectors were up over 1%, with Energy the only negative sector, which closed down hard by 3.66%. Airliners gained big on slumping oil prices while Delta posted positive earnings. Meta rose 6.5% after released its first AI model since founder Zuckerberg’s spending spree.

Asian stocks: Futures are mixed. APAC stocks rallied hard after the 2-week ceasefire announcement. Talks are set to start on Friday. The ASX 200 gained on outperformance in in gold miners and tech while energy slumped. The Nikkei 225 jumped above 56,000 with falling oil prices boosting sentiment while positive wages data also helped. The Hang Seng and Shanghai Composite benefitted from the upbeat mood.

Gold rose to a high at $4,857 and near 4-week high before retracing back near to the day’s lows. Prices stayed above 100-day SMA at $4651. Treasury yields drove the mood as they reversed some of their losses through the day.

Day Ahead – Post ceasefire announcement

Questions remain around the ceasefire agreement. It’s not clear that both sides are on the same page regarding the details of the truce, while attacks continued in the region and Iran is reportedly insisting that its permission is still required to pass the Strait. That said, after weeks of uncertainty, markets have seized on peace with huge moves in oil especially notable. Yesterday’s fall ranked in the top five biggest intraday moves since 1990 in Brent, with only the Kuwait invasion in 1991 and pandemic moves greater than this historic move.

We are now closely watching ship flows through the Strait of Hormuz, where a significant pick-up in volume would weigh further on oil prices and further boost risk taking. It would also reverse the stagflationary investment trends witnessed in markets over the last month that include the stronger dollar and weaker stock markets. But as said earlier, the 10-point plan delivered by Iran via Pakistan looks tough to agree upon, at least in the next two weeks. That was the path to an off-ramp as we predicted but expect volatility the closer we get to the next deadline. That could again mean we see Trump’s maximalist, escalate to de-escalate strategy which is the POTUS’ modus operandi. Wiser people than us appear to forget this!

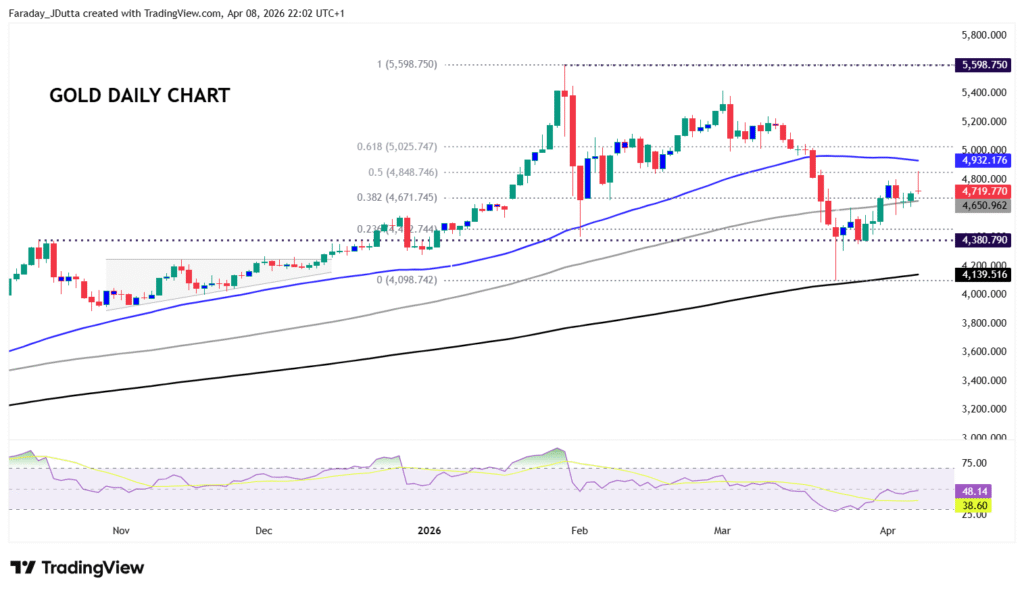

Chart of the Day – Gold break higher stalls

Gold’s safe haven qualities against uncertainty in the world have been questioned in recent weeks. That trade worked until just a few days after the Middle East conflict broke out, and then the correlation flipped. Since early March, the precious metal rose in response to hopes for a deal and declined when the fighting intensified. This was due to markets focusing on inflation concerns, rising yields and the dollar. The precious metal is non-interest bearing, and the rise in Treasury yields made it less attractive. Going forward, yields should typically move in a more orderly fashion, which should reduce their impact on bullion. That would allow a reversion to gold’s traditional haven role.

Technically, the precious metal faces resistance at the midpoint of this year’s high to low at $4,848 and then the 50-day SMA at $4.932. Support is the 38.2% retracement level at $4,671 and the 100-day SMA at $4,650. We note that even during its largest fall in mid-March, gold held above the 200-day SMA, currently at $4,139, which is another bullish sign for the long run.